Do I Have Gap Insurance? Quick Assessment for Peace of Mind on the Road

Ever driven a brand new car off the lot, only to imagine the financial nightmare if it were totaled in an accident? This is where GAP insurance comes in – a potential financial lifesaver for car owners with a loan or lease. But navigating the world of auto insurance can be confusing, especially when it comes to add-on coverages like GAP.

This guide provides a quick assessment to help you determine if GAP insurance makes sense for your situation, along with valuable insights for those with some existing knowledge.

Understanding the GAP: Depreciation vs. Loan Balance

The key to understanding GAP insurance lies in the concept of depreciation. Cars lose value rapidly, especially in the first few years of ownership. This phenomenon can create a “gap” between what your car is worth (its current market value) and the amount you still owe on your loan or lease.

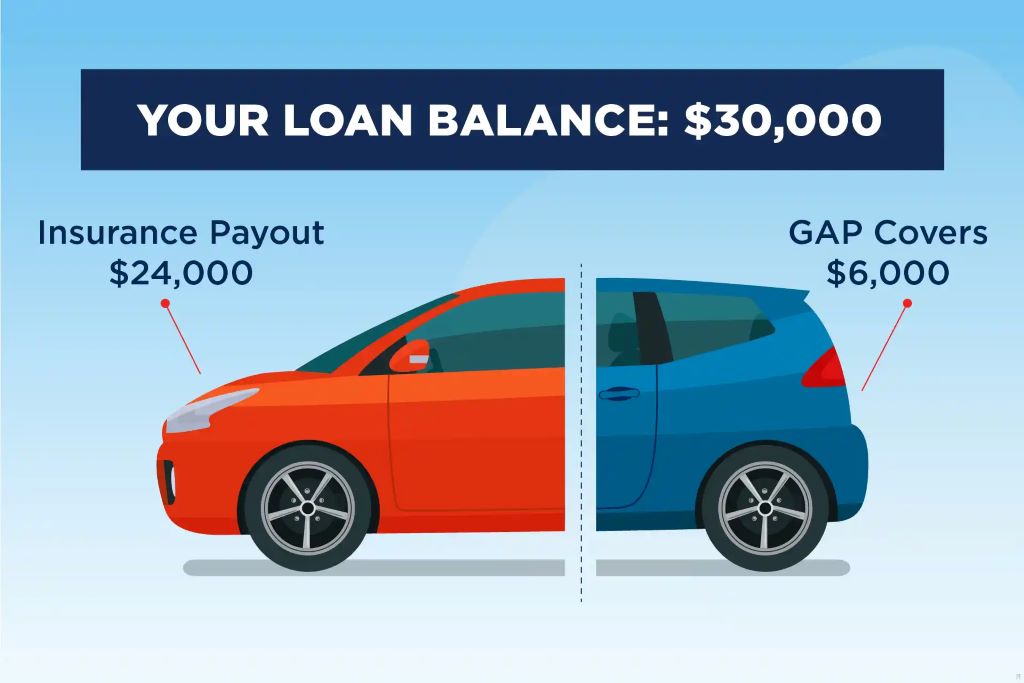

Here’s an example: Let’s say you buy a brand-new car for $30,000 and finance it with a loan. Two years later, the car’s market value might have dropped to $22,000. However, you might still owe $25,000 on your loan. In this scenario, if your car is totaled in an accident, your standard auto insurance policy would only pay you the car’s current market value ($22,000). You’d be left on the hook for the remaining loan balance ($25,000) – a significant financial burden.

Enter GAP Insurance: Bridging the Financial Gap

This is where GAP insurance steps in. It acts as a financial safety net, covering the difference (the GAP) between your car’s actual cash value (what your insurance company pays) and the amount you still owe on your loan or lease.

Do You Need GAP Insurance?

Here’s a quick assessment to help you decide:

- Loan or Lease: This is the biggest factor. If you have financed or leased your car, GAP insurance is generally recommended, especially in the early years of ownership when depreciation is most significant.

- Loan-to-Value Ratio: A high loan-to-value ratio (meaning you owe more on your car than it’s worth) increases your risk of ending up upside down in the event of a total loss. GAP becomes more crucial in this situation.

- Length of Ownership: New car owners benefit most from GAP coverage due to faster depreciation. However, even for slightly used cars, GAP can provide valuable protection.

Cruising Without the Wheels: A Guide to Car Insurance Without Owning a Car

Beyond the Basics: Valuable Insights for Informed Decisions

Now, let’s delve deeper for those with a basic understanding of GAP:

- Types of GAP Insurance: There are two main types:

- Original Equipment Manufacturer (OEM) GAP: Covers the difference between the car’s original purchase price and the loan balance.

- Replacement GAP: Pays the difference between the current market value and the cost of replacing your car with a comparable model.

- Cost of GAP Insurance: Premiums vary depending on the type of coverage, car value, and lender. Generally, GAP is more affordable than covering the potential out-of-pocket expense in case of a total loss.

- Alternatives to GAP: Consider increasing your comprehensive and collision coverage limits to get closer to your car’s value. However, this might not fully cover the loan balance and could increase your overall premium.

- Who Sells GAP Insurance: GAP can be purchased from your car dealer, insurance company, or a third-party provider. Compare prices and coverage details before making a decision.

- When to Cancel GAP: As your loan balance decreases and your car’s value approaches it, GAP becomes less necessary. Review your coverage periodically and consider canceling when the gap narrows significantly.

Related: How Much is Car Insurance Per Month

The Final Word: Peace of Mind on the Road

Ultimately, the decision to get GAP insurance comes down to your financial situation and risk tolerance. For those with a loan or lease, especially on a new car, GAP provides valuable peace of mind. By knowing you’re protected against the financial burden of a total loss, you can focus on enjoying the ride.

Remember:

- Regularly review your auto insurance coverage and consider GAP if it aligns with your needs.

- Shop around and compare prices before purchasing GAP.

- Don’t hesitate to ask your insurance agent or trusted advisor for guidance.

By taking these steps, you can ensure you have the right auto insurance coverage to navigate the road ahead with confidence.